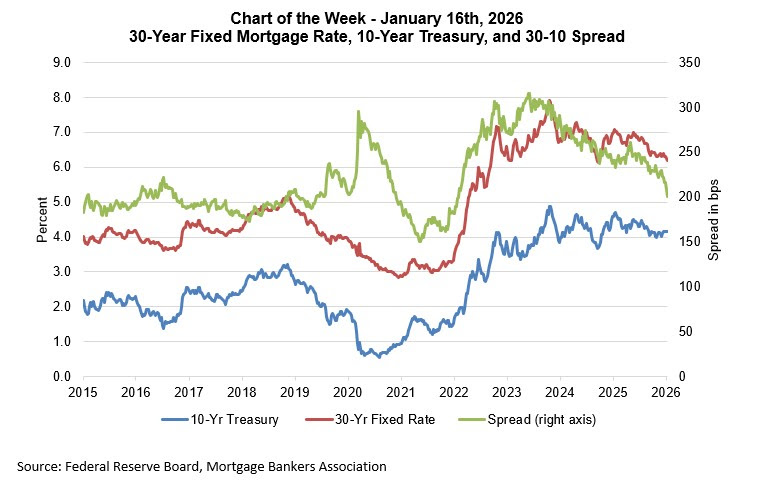

The spread between mortgage rates and Treasury rates is impacted by several factors, including the level of interest rate volatility and the relative demand/supply balance of the two types of securities. In recent months, rate volatility has diminished, as the future course of monetary policy has become clearer and financial markets have been relatively calm. Last week’s announcement that the GSEs will increase their purchases of MBS brought the spread in further, and mortgage rates dropped further over the course of the week.

Treasury rates have been quite stable over the past year; the 10-year Treasury has remained just below 4.2 percent for the past month. Our forecast for 2026 is for the 10-year to remain within a narrow trading range. However, a narrowing spread between mortgage and Treasury rates has brought the 30-year fixed rate to and below 6 percent in recent days. The mortgage-Treasury spread narrowed to 201 basis points for the week ending January 9th, down from 209 bps the week before and below the average spread of 220 bps for the month of December. The narrower spread led to decrease in mortgage rates, including a 15-bps decline in the 30-year fixed rate to an average of 6.18 percent last week.

The immediate impact was that refinance applications surged last week, jumping 40 percent to the strongest weekly pace since October 2025 in response to these lower rates, as many borrowers with higher rates or large loan sizes remain attuned to such downward rate moves. Purchase applications also rose last week and were up 13 percent ahead of last year’s pace, as lower mortgage rates and higher inventory kept potential homebuyers active in the market.

However, the initial reaction to the announcement regarding MBS purchases may overstate the longer-run impact. Other investors in MBS might see this market move as an opportunity to sell, which would push the spread wider. Surveying a range of market estimates, our view is that spreads might wind up about 10 basis points tighter than they otherwise would have been due to these purchases. However, there is considerable uncertainty as the size, pace, hedging, and financing strategies of these purchases have not yet been revealed, and these details matter regarding the ultimate impact. There is also uncertainty about whether the caps on the GSE mortgage portfolios might be lifted at some point.

{kind=link}

{kind=link}